Updated June 2026

What Is Collision Coverage Insurance?

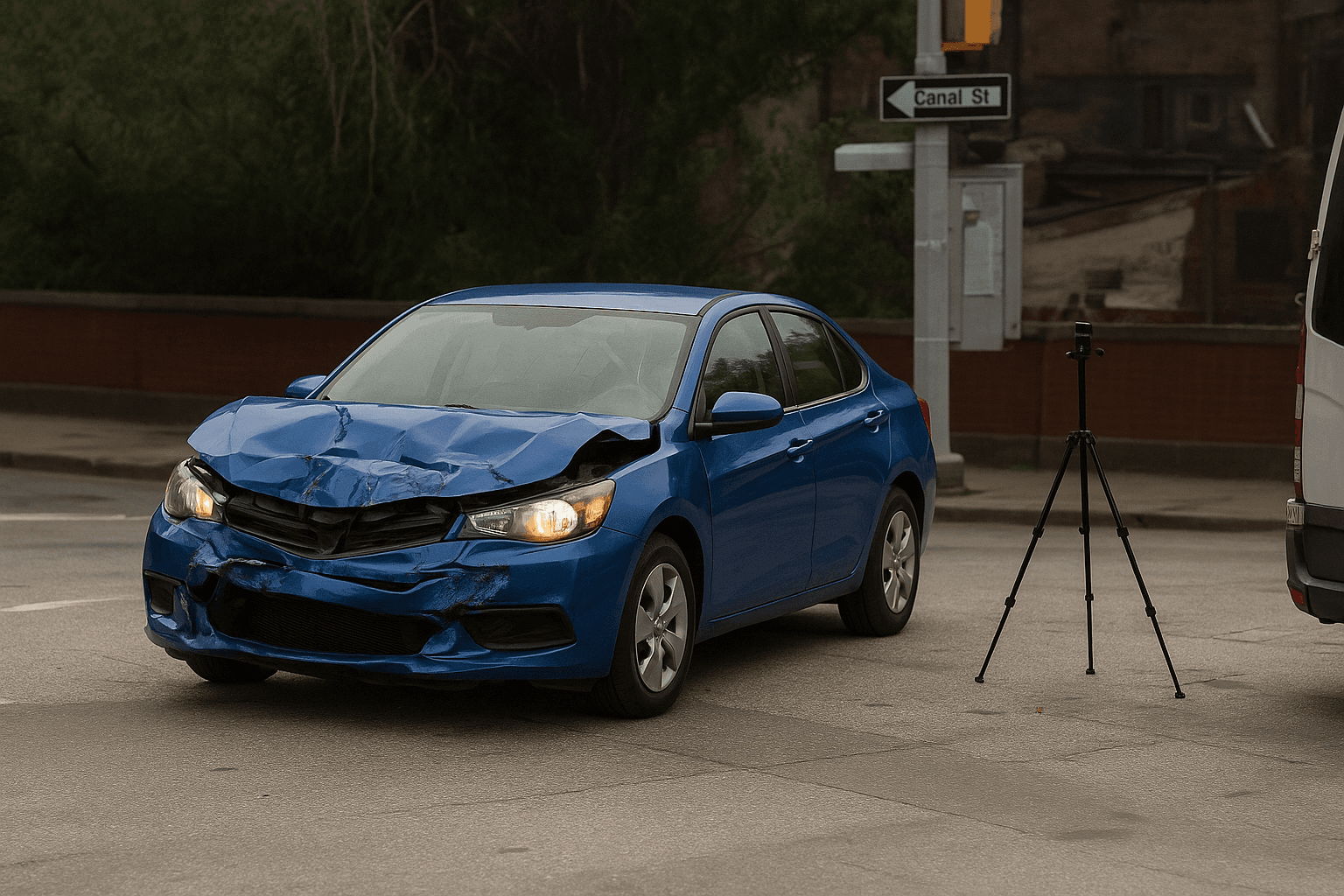

Collision coverage repairs or replaces your vehicle after a crash with another car, a guardrail, a tree, or any fixed object. It pays regardless of fault — even if you caused the accident. The insurer pays actual cash value minus your deductible, not the cost to buy an equivalent car at today's prices. If your 2014 sedan has a market value of $6,200 and you carry a $1,000 deductible, a total loss pays $5,200.

- You brake too late at a red light and hit the car ahead. The other driver has $3,400 in vehicle damage. Your car needs $5,800 in repairs. Liability covers the other driver's $3,400. Collision covers your $5,800 minus your deductible. If you carry a $500 deductible, you pay $500 and collision pays $5,300.

- A deer runs onto the road. You swerve, miss the deer, and hit a guardrail. Damage totals $4,200. No other vehicle is involved. Liability doesn't apply because you didn't damage someone else's property. Collision pays $4,200 minus your deductible. If your deductible is $1,000, you receive $3,200.

- You're in a multi-car accident. Your 2016 SUV is totaled. Market value is $9,800. You carry a $500 deductible. Collision pays $9,300. That's the settlement — not enough to buy a similar vehicle at a dealership, where comparable models list for $13,500. The gap between actual cash value and replacement cost is your responsibility.

Who Needs Collision Coverage Insurance?

Collision coverage makes sense if your vehicle's market value exceeds three to four times your annual premium for the coverage. A car worth $12,000 with a $600 annual collision premium justifies the cost. It's also necessary if you lease or finance — the lender requires it. Retirees who drive infrequently but own a vehicle worth $10,000 or more often keep collision with a higher deductible to lower the premium.

Calculate your vehicle's current market value using Kelley Blue Book or a similar tool. Divide that value by your annual collision premium. If the result is less than 5, consider dropping collision or raising your deductible to $1,000 or higher. If you drive fewer than 6,000 miles per year and your car is paid off, the math often favors dropping collision and banking the savings.

How Much Does Collision Coverage Insurance Cost?

Collision coverage typically adds $30 to $75 per month to your premium, or $360 to $900 annually, depending on your vehicle value and deductible.

- Vehicle age and market value — a 2012 sedan with a $4,500 value costs less to insure than a 2020 model worth $18,000.

- Deductible selection — choosing a $1,000 deductible instead of $250 can cut collision premium by 30 to 40 percent.

- Driving record — an at-fault accident in the past three years raises collision premium more sharply than liability premium.

- Annual mileage — drivers logging under 5,000 miles per year often qualify for low-mileage discounts that reduce collision cost by 10 to 20 percent.

- ZIP code claim frequency — areas with higher collision claim rates per capita pay more, even for drivers with clean records.

- Vehicle safety features — cars with automatic emergency braking or collision warning systems may qualify for rate reductions of 5 to 15 percent.